Levi's Research

Let’s start by understanding Levi’s operating segments:

It’s imperative first to comprehend that Levi’s is not a complicated company. One could argue it’s a bit boring in terms of what it does. For us, value investors, this is a perfect trait. Remember, as value investors, we want to try and predict the future cash flows of a company. The easier the business model, the better.

Levi Strauss & Co brands:

Levi’s

Signature by Levi Strauss & Co

Dockers’

Denizen brands

Beyond Yoga (acquired in 2021)

Segments:

Levi’s Brands: Levi’s, Signature by Levi Strauss & Co., and Denizen Brands.

Other brands: Dockers and Beyond Yoga.

Revenue share:

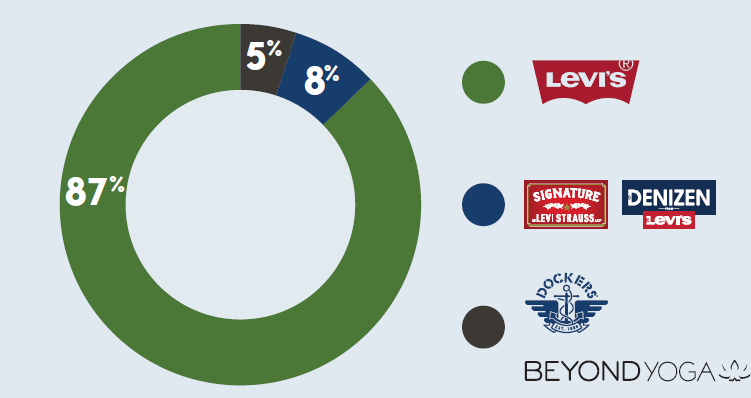

Revenues are concentrated within Levi’s brand; the brand made 87% of total revenue for 2021.

Global reach and Channels:

The company’s products are sold in more than 110 countries. Over half of the net revenue came from outside the United States in fiscal 2021. In the current environment, this would be a problem. *A higher dollar hurts companies with revenues coming in from abroad. This could become a tailwind once the dollar starts falling against other currencies.

Products are sold worldwide in approximately 50,000 retail locations, including ~3,100 brand-dedicated stores and shop-in-shops.

This is a critical piece of information; it comes to stress that the brand is growing due to higher demand and not expansion, which means that the company is not entering a new region. But more people are drawn to the brand to buy their product. The goal is to maintain market share leadership in Levi’s men’s and grow market share in Levi’s women’s and youth. The company also reached saturation levels. It is spread out internationally; growth would be stable. Buying this business at a fair price could be a golden opportunity for the next 5-10 years.

DTC push:

DTC’s business has grown since 2011. From 20% of net revenues to nearly 40% of the company’s net revenues in the fiscal year 2021. LEVI is trying to grow this segment to 60% of annual net revenues. The push would help LEVI cut the middle person and increase margins.

Financial Discipline:

The company wants to have an EBIT margin of above 12%. For the fiscal year ended November 28, 2021, Levi’s adjusted EBIT margin grew 12.4%. EBIT is earnings before interest and tax. The EBIT comes to show us how profitable a company’s operations are. Although interest and taxes are cash expenses, we exclude them because the company’s core business operations do not generate them.

Levi’s brand products dominance:

Levi’s brand products accounted for 87% of the company’s net revenues each fiscal year: 2021, 2020, and 2019. Half of the revenues were generated in the Americas segment.

Wholesale customers:

Sales to the top ten wholesale customers for the fiscal years 2021, 2020, and 2019 totaled 32%, 29%, and 26% of the company’s net revenues in those fiscal years. The good part is that no single customer represented 10% or more of the company’s net revenue.

Tailwinds:

Seasonality of Sales:

The fourth quarter is THE quarter for Levi’s. An upcoming tailwind would be Thanksgiving day. According to their 10K, the business achieves significant revenue from the DTC channel on Black Friday.

Cotton:

The primary fibers used in the majority of the products include cotton. The price fluctuations impact the cost of goods. Cotton price has been dropping, which is expected to lower LEVI’s costs.

Tourists:

In their last earnings call, LEVI mentioned that they benefited from a return of tourist traffic in many of their downtown locations which led to increased growth in their key cities, including San Francisco, New York, Paris, and London.

Long-term plans:

Levi plans to grow revenues in the range of 6-8% annually and achieve an adjusted EBIT margin of 15%. Return 55%-65% of free cash flows to shareholders.

Looking at data from the last quarter, revenues grew 20% to $1.5 billion. The growth is mainly driven by the U.S. markets. Supply chain-related issues limited growth by 2%. These issues will be resolved in the future.

Adjusted EBIT reached 9.9% despite rising inflation and foreign exchange headwinds.

The company also returned $80 million of capital to shareholders through higher dividends and the repurchase of 2 million shares.

Second quarter growth was primarily driven by higher volume and an increase in AURs (Average unit retails) (price).

Past performance does not guarantee future results.

Recently retailers in the U.S. mentioned that sales were slightly softening. According to Chip Bergh, the CEO of Levi’s, there is some evidence that low-income consumers are starting to feel the squeeze in inflation. Yet, he added that Levi’s is still doing well, mentioning Red Tab at Target.

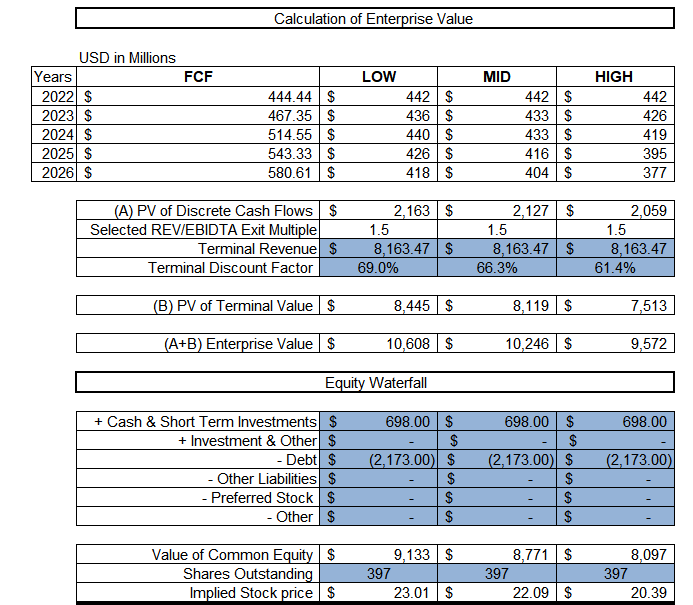

Valuation - DCF:

Revenues and EBITDA margins:

In this model, I assumed that revenues would be $6.4 billion for 2022, at par with analysts’ estimates. For 2023 and beyond, I applied a growth rate of 5%-6.5%. I feel that this growth rate, on average, is neither too aggressive nor too soft for a company like Levi’s. And it also falls on the lower end of their estimates.

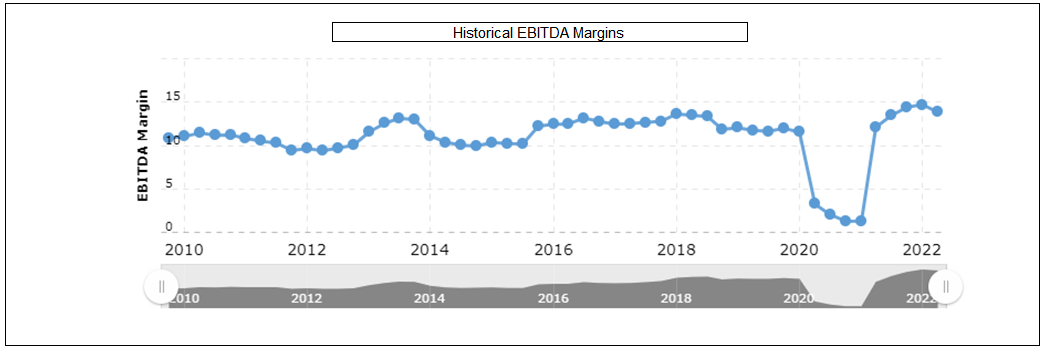

Regarding EBITDA margins, historic margins were used to indicate what future years will look like. Throughout this time, we can see that EBITDA was stable at around 13% and approaching 15% in some cases. I applied a margin of 13% for the years ahead.

Discount rates of 9%, 10%, and 12% for the Low, Mid & High, respectfully.

Cash flows as shown in the table. Again you can apply for more aggressive numbers here.

Per share price of $23 $22 & $20. Which is still higher than the current market price.

Disclaimer:

All investment strategies and investments involve the risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or a guarantee of any specific outcome or profit.