Disney Research

Let’s start by understanding Disney’s operating segments:

Disney Media and Entertainment Distribution DMED

Disney Parks, Experiences, and Products DPEP

Disney Media and Entertainment Distribution DMED

When we mention DMED, these are the subsegments that fall under this category:

1.1. Linear Networks

1.2. Direct to Consumer

1.3. Content Sales/Licensing

1.1. Linear Networks: Disney owns channels like Disney, ESPN, National Geographic, Fox, and more. Disney makes money from this segment through Affiliate Fees. They charge cable, satellite, and telecommunications service providers to deliver Disney’s programming to their customers.

1.2. Direct to Consumer: This subsegment is Disney’s latest push toward growth. Disney created Disney+, ESPN+, Hulu, and more. In this subsegment, Disney makes money by advertising and subscription fees.

1.3. Content Sales/Licensing: Disney sells or licenses films and television content to third-party television and subscription video-on-demand services. For example, they can charge Netflix to stream a Disney movie on its platform. Furthermore, they make money by releasing movies, stage plays, and more.

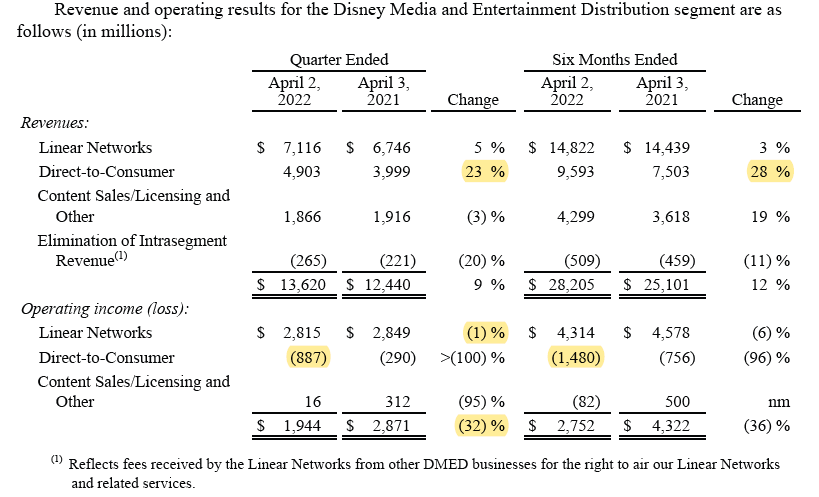

As said above, Direct-to-consumer (DTC) is the only subsegment in the DMED segment that offers double-digit growth. Looking at Q2 results, we can see that DTC grew 23% sequentially and 26% for the six months ended in April 2022 vs. April 2021. The growth is coming at a cost; in the “Operating Income (Loss),” we can see that Disney lost 887 million on DTC for Q2, growing from a loss of 290 million year over year and losing $1.4 billion for the six months ended in April 2022 dragging the whole operating income down by more than 30% for the three months and six months ended in April 2022. The increase in losses results from higher losses at Disney+ and ESPN+ and lower operating income at Hulu.

The bright spot here is that the subscriber count is growing in every single streaming service they offer:

Linear Networks, we can break this one down into Domestic Channels and International Channels. Disney saw strength within its Domestic Channels, where revenues increased 8% yearly, International channels revenues decreased 3%, and operating income decreased 30%.

Disney Parks, Experiences, and Products DPEP

This is Disney’s happiest segment as of right now. After the massive downturn in visitors due to Covid 19, Disney’s parks are finally getting busy again. We can see from the table above that for the second quarter this year, Disney’s Parks & Experiences revenues increased more than 100%, reaching almost $4.9 billion.

Here is what the CEO had to say about the Parks segment in the last earnings call:

As I said, our domestic parks were a standout. They continue to fire on all cylinders, powered by strong demand coupled with customized and personalized guest experience enhancements.

Now that we understand Disney’s primary operations, let’s take a look at the historical numbers:

From 2012 to 2021, Disney managed to grow its revenue steadily from 42 billion dollars annually to $69 billion in 2019. It compounded annual growth of about 5%, above the U.S. GDP. As of 2021, revenues grew from $65 billion in 2020 (Covid), reaching $67 billion. It is fair to expect Disney to grow its revenues at a pace of 5-6% yearly.

According to analysts’ estimates, Disney is expected to report revenue of $82.75 billion for the current year. Currently, Revenues for Disney YTD (Fiscal year) are $41 billion. It’s not farfetched to assume that Disney would bring another $40 billion in revenues in the last two quarters of the fiscal year, considering the tailwinds it’s experiencing from its park segment.

The chart above is not very accurate considering the last two data points I added: the current stock price and the estimated revenue for this year. That said, I believe it helps show the disconnect between the stock price, which is now at around $96 per share, while revenues are estimated to grow and reach $82 billion. That being said, operating, and net income is expected to grow this fiscal year. Regarding the stock price, I took the closest day to the end of each fiscal year and plotted it in this chart.

The chart below shows the daily price action from 2012 until the last trading session:

What are the expectations for the future?

Before diving into the future, let’s look at the current P/E ratio. As of the last trading session, the P/E ratio is 66x. This high P/E multiple doesn’t imply that the stock is expensive—the high multiple results from the unusual times we had during Covid. Looking at the forward P/E ratio (what counts in this case), we will see that the company trades at a 17 multiple.

DTC and valuation:

Disney ended the quarter with more than 205 million subscribers after adding 9.2 million. Disney aims to reach 230 million to 260 million Disney+ subscribers by fiscal '24. Remember that Netflix currently has 221 million subscribers, with an average revenue per user in the U.S and Canada of $14.91. For 2021, Netflix revenues were almost $30 billion. That said, market participants, value Netflix at approximately $80 billion with a P/E of 17.

I believe that Disney can provide better content and become a more sticky platform than Netflix. Yet, if we assume that Disney+ will become the next Netflix, we also think Disney+ or the whole DTC segment will generate $4.8 billion in net income on revenues of approximately $30 billion at some point. The real question is when it will happen and what the risks are.

This brings us to Aesop. A bird in the hand is worth two in the bush. Is it, though?

As of the last earnings report, for the previous six months ended in April this year, the DTC segment brought $9.5 billion in revenues with a net loss of $1.4 billion. For the average monthly revenue per paid subscriber, Disney+ charges only $6.32 in the U.S. and Canada. You bet they will increase the price.

To be an optimist, if Disney does manage to create the next Netflix in the next three to four years, we will buy Disney’s other operations (Parks, Trademarks, etc.) for around $95 billion if this is achieved.

Remember, the parks alone generated $6.65 billion in revenues last quarter. It wouldn’t be a surprise if Disney generated $20 billion in revenues from this segment by the end of the fiscal year.

To put those figures into context, in its last fiscal year before the outbreak, which ended in September 2019, this same segment generated $26 billion in revenue and $6.7 billion in operating income.

Tailwinds:

Parks & Entertainment:

As of the end of March, domestic amusement parks were open this year, with continued growth in parks. The two things that can stall this growth are another Covid outbreak or a recession. According to the CEO, they are still seeing strong demand. This, of course, can change; we will know it soon in their upcoming report.

Headwinds:

Recession, increased spending on DTC, Disney+ not reaching profitability.

Valuation - DCF:

Revenues and EBIDTA margins:

Here I assumed revenues would grow 21%, a bit lower than analysts predicted for 2022. Revenue growth for 2023 of 5%, as a result of a slowdown in the economy or even a recession. For 2024, I assumed that the growth would be 11% higher than the CAGR due to coming out of recession or economic slowdown. For 2025 and 2026, I assumed revenue would grow higher than the GDP growth around CAGR.

Regarding EBITDA margins, historic margins were used to indicate what the next years will look like. I Didn't pick the mid-teens/20's tried to stay conservative assuming EBITDA margins won’t grow back to where they were.

Discount rates of 9%, 10%, and 12% for the Low, Mid & High, respectfully.

Cash flows as shown in the table. Again you can apply for more aggressive numbers here.

Per share price of $86.51 $82.53 & $75.11.

Charlie Munger once said, we calculate too much and think too little. No one can know what happens next. With that being said, in my opinion, Disney has an enormous moat. There are many ways to tweak the above model and reach a higher share price where Disney would be undervalued at current prices. Since it’s a public valuation, I’d rather not be overly optimistic.

The relative valuation I made in the middle of the article comparing the DTC/DIS+ to Netflix shows that acquiring all of Disney’s assets besides this segment for around $90 billion is not expensive.

I hope you liked this; if you do, please like and share this article.

Disclaimer:

All investment strategies and investments involve the risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or a guarantee of any specific outcome or profit.